Review in Medium.com – Labor in the Age of Finance

Labor in the Age of Finance: A Review

09.09.22

Labor economist Sanford Jacoby is not read for his optimism. His latest release, Labor in the Age of Finance: Pensions, Politics, and Corporations from Deindustrialization to Dodd-Frank, begins with a grim pronouncement: “The 1970s and 1980s were a disaster for America’s labor movement. Gone were nearly one out of three members from private industry, once the heart of organized labor. Critics charged that unions had become dinosaurs: archaic and doomed. Facing slow extinction, leaders of several unions decided the time had come for a do-or-die struggle to renew and rebuild.”

How did labor remake itself? With a sudden “financial turn” in the late 20th century. Jacoby’s work chronicles how a weakening labor movement embraced, rather than rejected, an increasingly financialized economy, seeking to leverage workers’ vast pools of capital for strategic ends. The 1970s and 1980s witnessed a revolution in stock ownership from individuals to institutions. Public pensions and labor unions transformed from “sleepy bondholders” into active shareholders with large equity holdings, launching a full-scale rebuttal to postwar understandings of corporate governance.

“For most of the twentieth century, the worlds of finance and labor spun in separate orbits,” writes Jacoby. “They drew nearer as the century came to a close and a new one began… Finance-based pressure tactics, which included shareholder activism but went beyond it, became a regular part of campaigns to add members. The recurring corporate scandals of the 2000s, which angered the public and investors, put the wind at labor’s back. After the banking crash, labor’s regulatory agenda drew on its financial turn. It was a pretty good showing for an alleged dinosaur.”

What happens when labor unions — and their public pension fund allies — become some of the largest institutional investors? Can they preserve the wages and jobs of current workers while protecting the incomes of their retired members? Is there an inherent contradiction between the two goals? Can corporations credibly play a role in mediating economic inequality?

These are the questions Jacoby seeks to answer in his astonishing new work, the first comprehensive attempt to understand how the US labor movement adapted itself to “the creed of shareholder capitalism,” turning to pension fund activism, regulatory reform, and democratizing corporate governance to serve workers’ needs.

CalPERS Rewrites the Cookbook

Jacoby credits the California Public Employees’ Retirement System (CalPERS) with instigating a broader shareholder revolt across the nation. Contrary to the “old Victorian feeling that shareholders should be seen and not heard,” CalPERS led the way for a new brand of shareholder: one who directly challenged management and increasingly demanded a say in corporate governance.

The earlier postwar generation held no special place in its heart for shareholders. In the mid-1950s, a team of renowned economists — including Carl Kaysen, Seymour Harris, and James Tobin — sought to answer the question of how power should be exercised in public corporations. They interviewed a sample of executives from major corporations who consistently listed four broad responsibilities: “to consumers, to employees, to stockholders, and to the general public… In any case, each group is on an equal footing; the function of management is to secure justice for all and unconditional maxima for none.” The report found that “stockholders have no special priority; they are entitled to a fair return on their investment but profits above a ‘fair’ level are an economic sin.”

Yale political scientist Robert Dahl captured the broader political sentiment in his 1961 study of New Haven, Who Governs? “Why should people who own shares be given the privilege of citizenship in government of the firm when citizenship is denied to other people who also make vital contributions to the firm? The people I have in mind are, of course, employees and customers, without whom the firm could not exist, and the general public.”

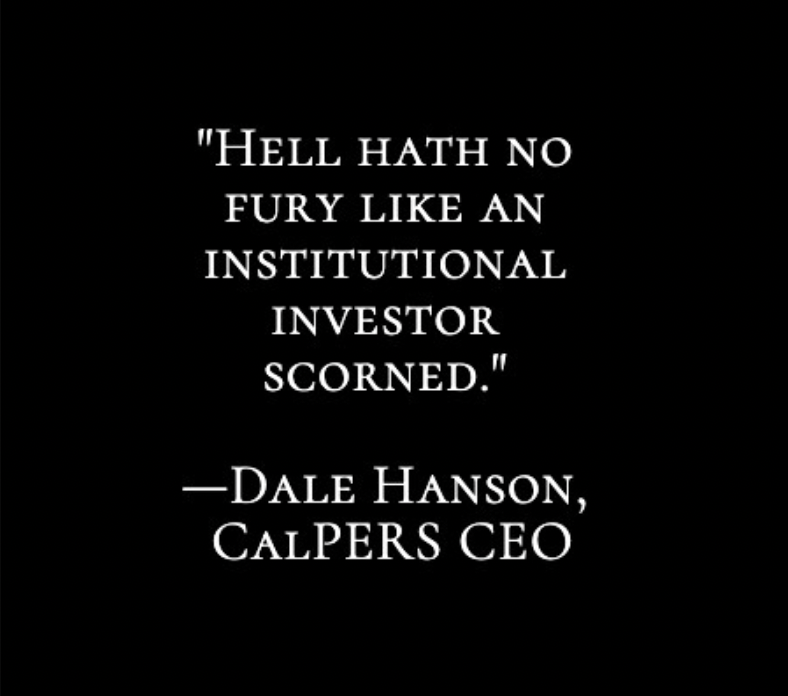

Dale Hanson, who took over the helm of CalPERS in 1987, flatly rejected this view and was aptly described by the New York Times as “an investor with an attitude.” He was known his mantra, “Hell hath no fury like an institutional investor scorned.” Hanson believed the best way to increase portfolio returns was to elevate the position of the shareholder. CalPERS devised three main demands to prioritize their interests: “tying CEO compensation to stock performance, orientating executives and corporate boards to shareholders, and lowering the barriers to acquisitions.”

Hanson began his memorable reign as a “governance kingpin,” asking companies to keep proxy voting confidential, leading a number of highly public campaigns to remove CEOs, and “demand[ing] the creation of shareholder advisory committees composed of large, long-term shareholders who would be invited to private meetings with directors.” CalPERS created a “Failing Fifty” list of companies with lagging returns (over a five-year period) where it intended to publicly shame them, file proposals, and meet with management and boards.

Business leaders were flabbergasted. As Hanson described it, such direct confrontation with directors and CEOs “was equivalent to flatulence in church.” Still, Hanson felt that he created meaningful change. In the 1980s, “if you were not Forstmann Little or KKR or Carl Icahn, shareholders were a joke,” he recalled. Now, shareholders could credibly make demands. “We learned the importance of meeting with directors,” said Hanson. “We wanted to see if there were any lights on — were they representing us and was there any accountability.”

In 1991, the AFL-CIO’s Pension Investment Committee released model proxy guidelines that drew heavily from CalPER’s so-called “cookbook” of corporate governance rules for inspiration. “What made the cookbook tolerable for unions was its premise that executives could not be trusted, a good fit to the labor movement’s gut instincts,” writes Jacoby. “When union power began to wane in the 1970s, so did corporate tolerance of what labor had wrought: job security, pension benefits, and steady pay increases. For union pension funds and for unions, ‘imperial executives’ were to blame for what had been lost.”

Prominent labor leaders, including Bill Patterson of the ACTWU (Amalgamated Clothing and Textile Workers Union) and Richard Trumka of the UMA (United Mine Workers), embraced the cookbook’s principles to demand more corporate accountability and to win better outcomes for labor (or so they thought). By 1995, the number of shareholder proposals submitted by union plans outnumbered those from public plans.

“What’s driving it for labor,” said one observer, “is a fundamental philosophical belief that management has a sinister reason for wanting to have classified boards and poison pills, which is to cover their own asses.”

Did the Cookbook Actually Work?

Was labor’s foray into financial activism worth it? Jacoby is ambivalent towards the results. On the one hand, much of the cookbook’s agenda — greater transparency, board member independence, and broader corporate accountability — was achieved. In 2016, TIAA-CREF co-authored an opinion piece in the Wall Street Journal announcing the triumph of the shareholder rights agenda.

Jacoby agreed with them, in some respects. “There was evidence backing up their celebratory claim,” he writes. “Ninety percent of the S&P 500 firms now relied on majority voting and had adopted annual director elections instead of staggered boards. The number of companies combining the CEO and chairman positions had dropped by half since 2001. Proxy access was widespread. Merely 4 percent of the S&P 500 maintained poison pills, once the bêtes noires of the cookbook.”

And yet, had labor’s position improved? In terms of inequality, the answer was a resounding no. While American firms were once berated by economists for “pay[ing] its most important leaders like bureaucrats,” executive pay was surprisingly contained from World War II through the late 1970s. Only when labor insisted on tying executive pay to stock prices did the wealth gap dramatically increase, undercutting some of labor’s longer-term goals. “The cookbook didn’t perform as promised because executives were able to subvert its intent,” writes Jacoby. “They could adopt the cookbook while cooking the books.” CEOs were, in essence, incentivized to go after their own workers, cutting costs, outsourcing labor, and reducing workforces to increase stock prices.

“The one sure thing that the cookbook produced was more power and money for shareholders and, via stock-based pay, for executives,” concludes Jacoby. “A study by a group of economists from Berkeley, MIT, and NYU finds that from 1989 through 2017, corporations created $34 trillion of real equity wealth. Nearly half of it was a reallocation from workers to shareholders.” Buybacks — now a common target for unions — were yet another example of the strange disconnect between retired shareholders and current workers: they “enrich CEOs and investors but are associated with lower levels of employment, investment, and wages.”

A Return to Managerialism?

After forty years of ascendancy, shareholder primacy is no longer taken as gospel today. In recent years, labor and business alike have showed a renewed interest in corporate reform. “Hipster antitrust,” aka the new Brandeis movement, is on the rise in popular culture, and, in 2019, the Business Roundtable — representing two hundred of the United States’ largest public corporations — issued a sharp rebuke to shareholders in its “Statement on the Purpose of a Corporation.”

The Roundtable confirmed its move “away from shareholder primacy [and] include[d] its commitment to all stakeholders.” Tellingly, shareholders were listed at the bottom of its list of stakeholders. “The corporations pledged to compensate employees fairly, provide them with benefits, train them, and treat them with dignity and respect,” writes Jacoby. “Shareholders were promised transparency, engagement with managers, and long-term value.”

Labor, for its own part, has weakened its marriage to shareholder activism: labor unions once accounted for 42 percent of corporate governance proposals (2003–2007), a percentage that has dropped to 13 percent in recent years (2015–2018). Whether this indicates a meaningful shift from shareholder primacy remains to be seen.

“In the past, organized labor raised living standards and shored up democracy. It can happen again,” writes Jacoby. But he qualifies this with the need for a new coalition more suited towards our own times. “The longue dureé of postwar capitalism rested on a commonweal of shared risk and prosperity, one of whose foundations was the labor movement,” he concludes. “Ours is a meaner era. Its hallmarks are staggering inequality and flat incomes for the vast majority. Improving the situation will require a host of changes: to shareholder capitalism, the tax system, social spending, and more.”

About Colbeck: Colbeck is a strategic lender that partners with companies during periods of transition, providing creative capital solutions to meet their evolving needs. You can reach the team at inquiries@colbeck.com.

© 2024 Sanford M. Jacoby. All rights reserved.

Created by